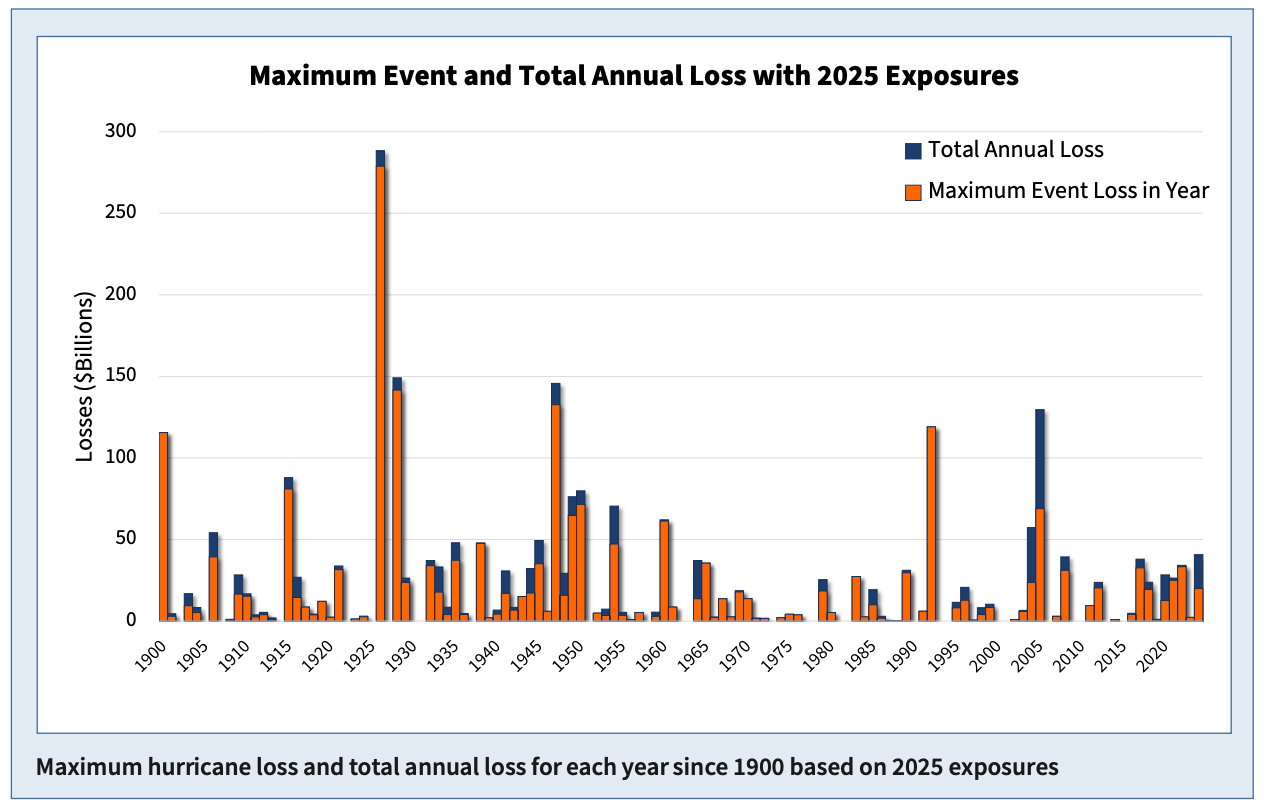

Were the 1926 Great Miami hurricane to occur again today, analysis from catastrophe risk modelling specialists Karen Clark & Company (KCC) suggests that more than $5 trillion in insured property value would be affected by hurricane force winds, driving well over $200 billion in insurance and reinsurance market losses.It’s a stark reminder that while we’ve seen some major hurricane loss events in the last couple of decades, they would pale into comparison with some of the largest historical events ever seen.KCC has looked at current insured exposure values and historical storm impacts and found that there have been four hurricanes that occurred prior to 1960 that if they happened today would result in over $100 billion in insured losses.The most recent would be hurricane Andrew in 1992, which would cause somewhere around $110 billion or so of insurance and reinsurance market losses if it struck today.

Two others are historical storms that struck southeast Florida and Galveston, that would also be $100 billion plus loss events today for the insurance industry.But it is the Great Miami hurricane of 1926 that would be the largest loss by far, with KCC’s data suggesting insurance and reinsurance losses would extend well-above the $200 billion mark, with the chart from its latest report suggesting as high as perhaps $275 billion.It’s a good reminder that while we’ve seen very impactful hurricane seasons of late and we often talk about reinsurance, catastrophe bonds and insurance-linked securities (ILS) structures being tested by storm seasons, a real test of that scale has not happened in almost a century.

KCC commented, “One hundred billion dollar events can occur where there are large concentrations of coastal population and property values, such as the Florida Tri-County area, Galveston/Houston, and the Northeast.” When the Great Miami hurricane struck that city had a population of just 100,000, where as today it is over 6 million.KCC explained, “If this storm were to occur today, over $5 trillion in total property value would be impacted by hurricane-force winds.“While building codes and construction practices have improved since 1926, given the storm’s strength and landfall location, the insured losses today from a repeat of the Great Miami Hurricane would exceed $200 billion.” There are modelled scenarios of Category 5 hurricane landfalls for the Galveston region of Texas that would also drive insured losses well-over $200 billion, so it’s not just Florida.

KCC notes that it is location that matters here.“The most important determinant of insured losses from hurricanes is landfall location.Shifting the landfall point by only 10 miles can make a big difference in industry as well as individual company losses,” the company explained.

Adding that, “From an industry perspective, the US has been lucky over the past few decades as a major hurricane has not made landfall in a densely populated metropolitan area.With the build up of coastal exposures, a $100 billion insured loss is not only possible, but likely today.” It’s worth thinking about what a $200 billion plus insured hurricane loss might mean for the catastrophe bond and ILS market.Such an event would cause meaningful losses to ILS structures, across the full-range of offerings the market employs.

While losses more broadly across the reinsurance and retrocession market would be even more significant.Capital would be depleted for many insurers and reinsurers, while ILS structures they utilise would provide very welcome relief in terms of the payouts they provided.A hard market would no doubt ensue, after such a significant depletion of dedicated reinsurance and ILS risk capital.

It would change the market dynamics, in terms of the way capital was raised, we suspect.Opening the door to start-up reinsurance company capital raises, but also with capital markets and ILS structures being able to demonstrate that they provide efficient mechanisms to replenish capital and protection.Which structures provided the recapitalisation after such a major event would be intriguing to see.

For investors into catastrophe bonds, ILS and other property cat exposed reinsurance structures, the losses would be meaningful.But the ability to recapitalise and trade forwards would be critical at that time for the insurance and reinsurance market, so we suspect many investors would be keen to demonstrate their stickiness and refund structures to provide continuity to their counterparties while benefiting from what would clearly be a generational hard market in pricing terms..All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance can be accessed online.

Our can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.

Disclaimer: This story is auto-aggregated by a computer program and has not been created or edited by Health Insurance USA.

Publisher: Artemis

Publisher: Artemis