Catastrophe bond pricing remains firmly in the “neutral zone” according to the latest analysis from consultancy Lane Financial LLC, but the firm maintains its prediction that the market is still on-track for an expected 8.5% total return in 2025.Lane Financial had forecast earlier this year after Q1 that .So far, the level of losses (actual and mark-to-market) remains within expectation, for an average year, the consultancy explained in its latest paper, while at the same time price development in the catastrophe bond issuance marketplace remains aligned with Lane Financial’s 8.5% after losses forecast.

Notably though, while yields have risen over the second-quarter of 2025, they have not done so as much as might have been expected in a typical year.Morton Lane and Roger Beckwith of Lane Financial write, “The onslaught of issues this quarter has caused yields to rise on Nat Cat ILS.However, not as much as one would expect.

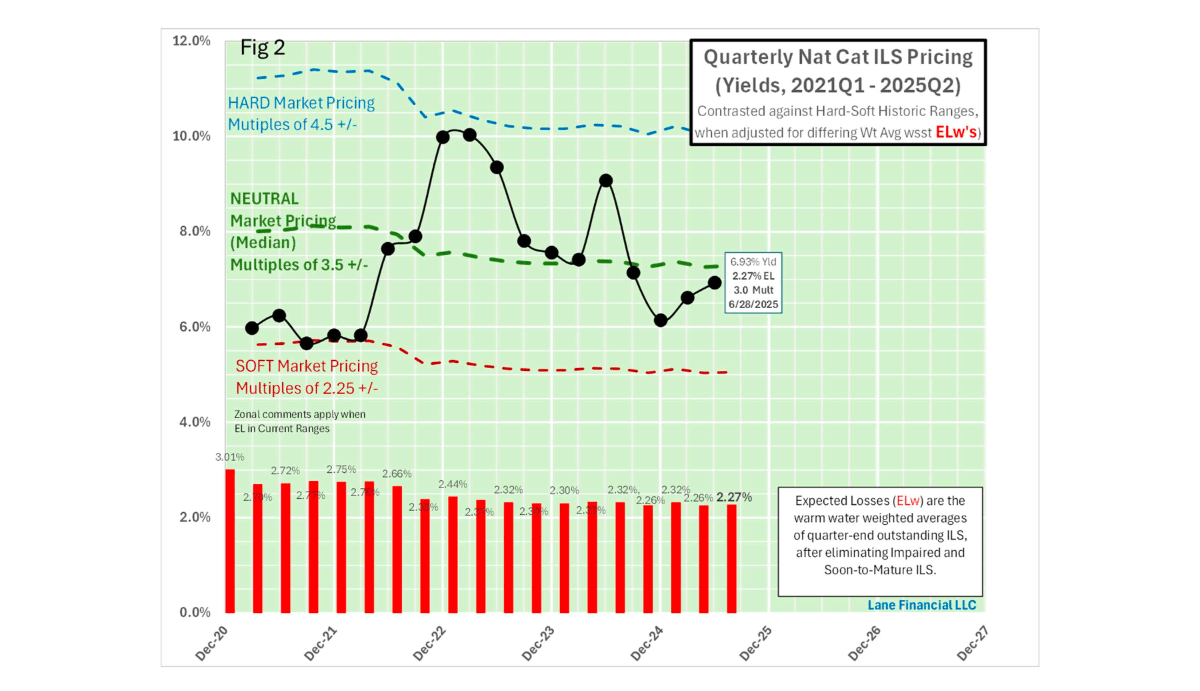

Since ILS issues cluster around the period just before the onset of the Hurricane season on June 1st, there is a seasonal dip in prices, i.e., a seasonal rise in yields.“This year, 2025, weighted average yields for the end-of-quarter market portfolio (i.e., excluding impaired securities and soon-maturing ones) have risen from 6.61% at end-Q1 to 6.93% at end-Q2.That is a 4.8% increase or if you prefer, an increase of 32 basis points.” However, the average seasonal shift from Q1 to Q2 yields in the catastrophe bond market is more typically 14% and Lane Financial attributes the reduced yield-gain in 2025 to .

“Clearly, the average pattern is a rise of nearly 15% – three times as much as this year.In essence, huge supply was met by a more-than-adequate appetite by investors.This is true even though the average issue date is getting earlier and earlier in the year.

Once upon a time, spring issuance was balanced by fall issuance and the weighted average issue date was in August, now it is mid-June.That could explain some of the extra supply this quarter but it is unlikely to account for a lot,” the consultancy explains.Leading Lane and Beckwith to conclude, “Given existing yields, what the market is predicting for expected returns at year end is the same 8.5% that was suggested at the end of Q1.

The math is simple as usual.Expected losses rose a basis point to 2.27% so the expected underwriting return is 4.66% (=6.93%-2.27%).To this we must add the floating rate.” The Lane Financial analysis includes some allowance for a declining risk-free rate of return on collateral, due to the potential for further US rate cuts in 2025.

So they took 3.875% as a mid-point for the floating rate to get to the 8.5% forecast expected total return for the cat bond market.The consultancy cautions that this is based on losses falling within expectation, warning that due to losses “the actual return can deviate markedly from expected return.” Of course that means if losses come in below expected modelled levels then the total return of the market could be higher and if some of the marked-down cat bonds were to recover that could also have an effect.Currently, if the models are to be taken as gospel, the expected loss of the catastrophe bond market implies annual losses of around $1.154 billion, the Lane Financial analysis shows.

The firm’s analysis also presents charts that show how market pricing is developing, on which they conclude, “They all reinforce the basic message that at this pricing, prices are in the neutral zone.” The chart below, taken from the paper, shows the average spreads on offer with catastrophe bonds continuing to rise into the second-quarter of 2025, but not as much as seen in some other years, as Lane Financial explained.Cat bond pricing remains just south of neutral as a result, but still above what would be termed soft market levels by Lane Financial.For an alternative view you can analyse the .

As of June 27th 2025 the implied return of the cat bond market after accounting for an expected level of catastrophe losses (by subtracting the expected loss) is slightly higher at 8.76%.However, incorporates the current risk-free rate from a source of its choosing, at a collateral yield of 4.3%, which is higher than Lane Financial approximation for where the floating-rate of return may sit later this year.The new paper is not yet available on the Lane Financial website, but and ask if you would like a copy..

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance can be accessed online.Our can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.

Disclaimer: This story is auto-aggregated by a computer program and has not been created or edited by Health Insurance USA.

Publisher: Artemis

Publisher: Artemis